Booze stocks are having a party. Should you raise a toast? MakkalPost

The list of those preaching abstinence, in fact, is a long and distinguished one. Investing legend Charlie Munger listed liquor as among the three ways a smart person can go broke (the other two being ladies and leverage).

But as Berkshire Hathaway’s investing activities over the years demonstrated, there’s a difference between consuming alcohol and investing in it. And sometimes, the difference can be a prodigious one.

While Dalal Street is being buffeted by consumption headwinds and geopolitical gyrations, liquor stocks are having the time of their lives.

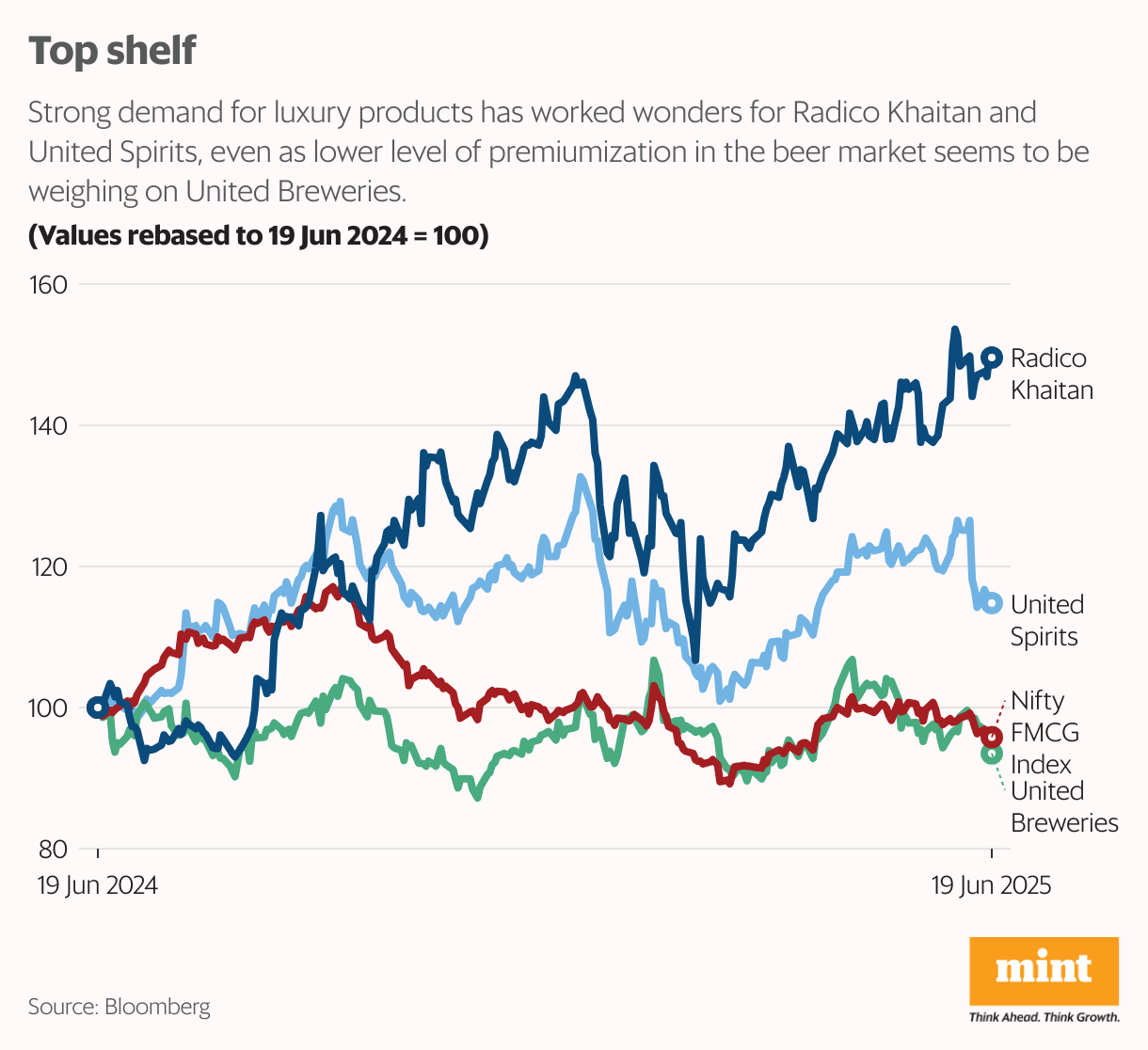

The top two performing stocks in the Nifty FMCG index over the past year are Radico Khaitan and United Spirits.

Not just that, the outperformance is the size of a Patiala peg. While Nestlé India and HUL have shed up to 8% over the past 12 months, Radico Khaitan has soared 50%, and United Spirits is up 15%.

Even beyond the FMCG index, smaller players like Allied Blenders & Distillers, Tilaknagar Industries and Som Distilleries have jumped around 35% each.

Bottoms Up!

What explains this joie de vivre?

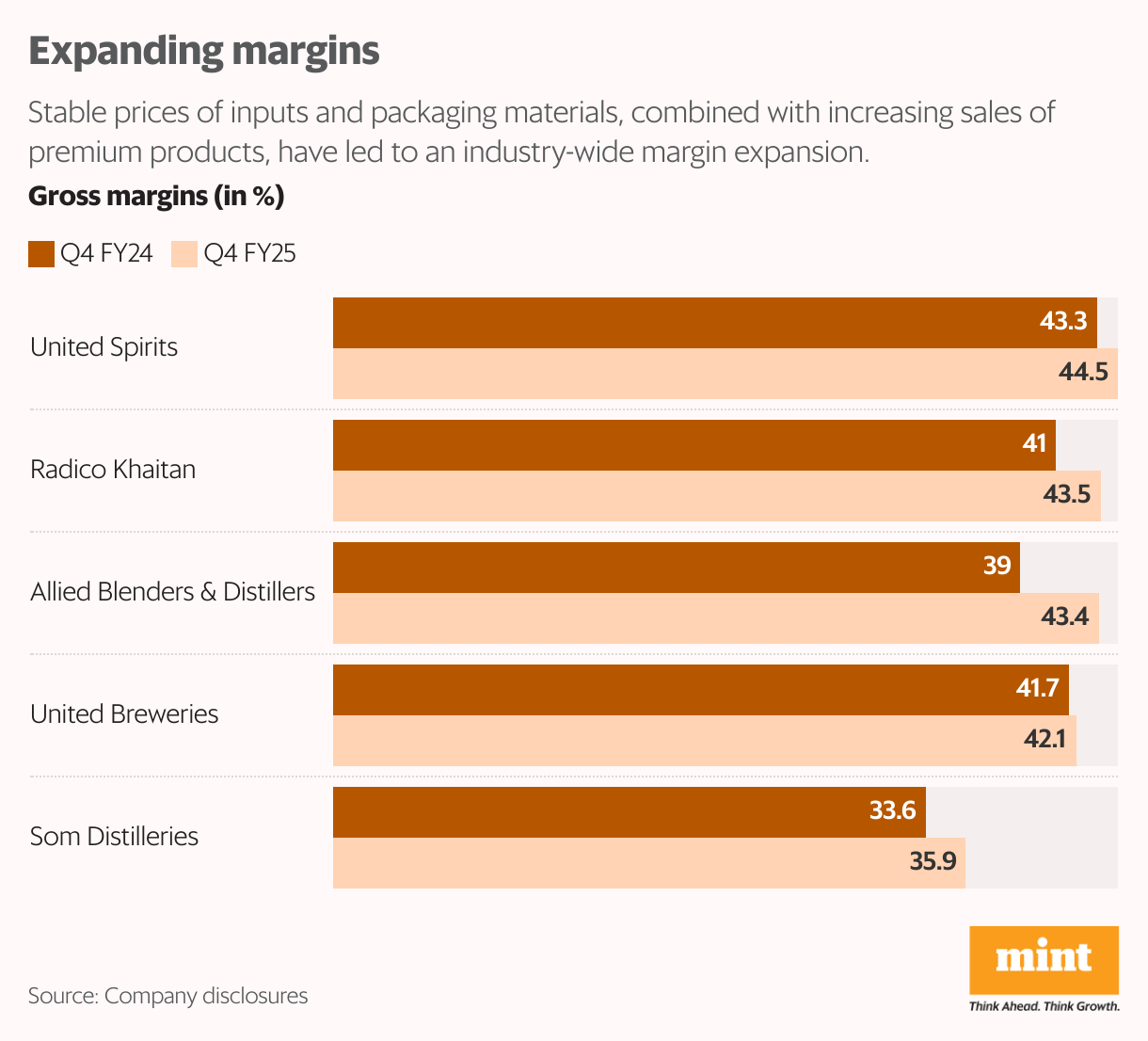

“A lot of factors are aligning favourably for the sector at this juncture,” Ajay Thakur, research analyst at Anand Rathi Institutional Equities, told Mint. “Firstly, prices of raw materials like ENA (extra neutral alcohol) are currently benign. Secondly, companies’ premium portfolios are doing extremely well. Which means alcohol companies are seeing robust margin expansion, which is leading to the stocks being re-rated,” he said.

Not just that, the current domestic regulatory environment also looks conducive. The recently signed India-UK Free Trade Agreement (FTA), under which import duties on Scotch will be halved from 150% to 75% and further to 40% over the next 10 years, will give a fillip to high-end consumption. The Street is expecting anywhere between 25- 30% kind of earnings CAGR for alcohol companies over the next two years, he added.

India is now the fastest-growing alcohol market among the world’s top 10 liquor-consuming nations, even as global demand is seeing a dip, per data shared with Mint by London-based spirits consultant IWSR.

The country’s alcohol market grew 9% by value in 2024, reaching just under $40 billion, marking India’s entry into the top five by value last year.

Beer outpaced all other categories in India in 2024, while whisky continues to dominate, putting the country on a path to cross $50 billion in alcohol sales by 2031. India could even possibly dethrone France and the US as the world’s top Scotch market by volume by 2027, it added.

While aggregate numbers are striking, India’s low per capita consumption underscores the sheer headroom for growth.

Of the 160 markets that IWSR tracks every year, India is ranked 145th in per capita consumption of beverage alcohol. India’s per capita consumption is just 6% of that in the UK and Germany; 7% the amount in the US, and 8% the amount in Brazil.

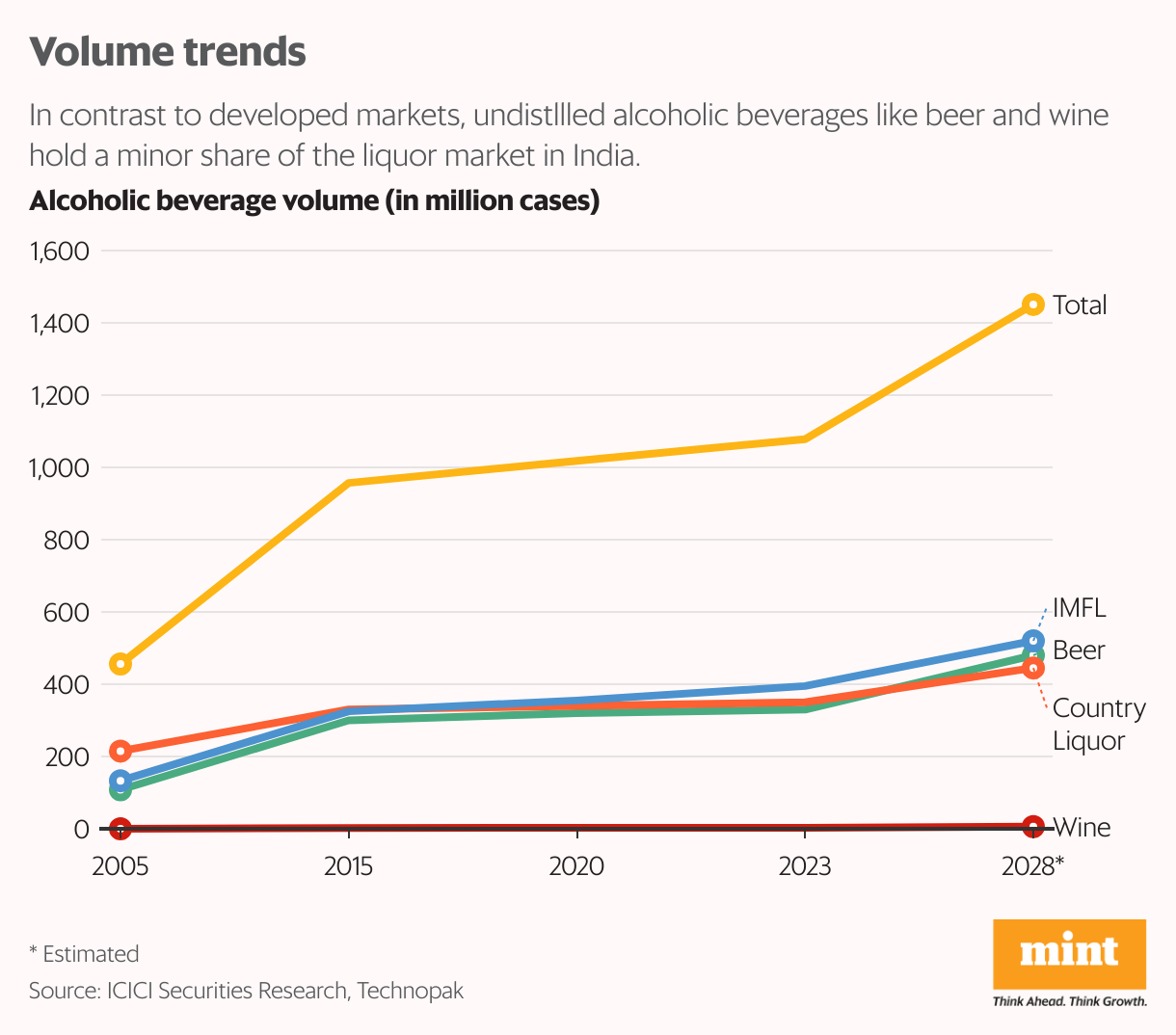

Alcohol consumption is segmented into three main product categories—spirits, beer, and wine.

India remains a predominantly distilled alcohol market, with around two-thirds of alcohol consumption comprising distilled spirits such as whisky, vodka and rum. This is in sharp contrast to developed nations, where undistllled alcoholic beverages such as beer and wine collectively hold a larger market share.

Within the spirits market, around 70% market share is held by Indian-made foreign liquor (IMFL) brands.

All alcoholic beverages manufactured in India that are not native to the country are called Indian-made foreign liquor (IMFL).

While foreign liquor like whisky, gin, scotch etc are made from traditional raw materials like grain using conventional techniques, IMFLs are usually produced from a neutral spirit (ENA) distilled from molasses, a byproduct of the sugar industry. This neutral spirit (at 96% alcohol by volume) is diluted using demineralised water, after which flavours and sometimes colour are added. However, many premium offerings, like single malt whisky, are made using the best quality grains. Sometimes, they are also blended with imported spirits like scotch.

Brown spirits (whisky, brandy and rum) dominate the IMFL segment, contributing around 96% of volume.

In value terms, the Indian alco-beverage market is categorized into four key segments: popular, prestige, premium, and luxury.

Popular brands are priced at up to ₹400 per 750 ml, while prestige category is priced at ₹400- ₹1,000. Premium and luxury spirits cost more than ₹1,000 and ₹2,000 per 750 ml, respectively. While the value segment (comprising popular and prestige labels) dominates the market, it is the premium category which is leaving analysts more stirred than their evening martinis.

Craft Connoisseurs

Perhaps the most conspicuous trend in India’s post-covid economy is the rise of luxury consumption. From FMCG to real estate and tourism, the unabashed rise of India’s uber-rich is changing the demand dynamics of a host of sectors. Including alcoholic beverages.

India is witnessing a growing acceptance of luxury liquor, driven by triggers like urbanization, younger generation reaching legal drinking age, higher disposable incomes and reduction in social taboo of drinking, ICICI Securities highlighted in a recent report.

“Incrementally, young consumers are willing to experiment with the liquor supported by innovative marketing by liquor companies. Additionally, the consumption of liquor in on-trade channels and increasing trend of social drinking is further aiding growth. The acceptance of Indian luxury liquor is no longer limited to the Indian diaspora; international consumers are increasingly seeking out Indian products,” it added.

From being considered the backwaters of the alcohol industry (a desi daru market), to creating luxury liquor brands which are among the most admired globally, India’s liquor companies have come a long way. There was a time when Indian whisky was not even considered worthy of the name as it was produced from molasses, not grains. A watershed moment came in 2010 when the Amrut Fusion single malt whisky, produced by the Bengaluru-based Amrut Distilleries, was ranked the third best whisky in the world by legendary whisky critic Jim Murray.

View Full Image

Over the years, the country’s luxury liquor offerings have gained steady market share, not just globally but also in a notoriously price-conscious market like India.

Frontline alcohol companies are seeing their prestige and above (P&A) segment growing faster than mass market brands. Radico Khaitan, which owns brands like Rampur, 8PM, Magic Moments and Royal Ranthambore, clocked volume growth of 15.5% in the P&A segment in FY25 over the year-ago, compared to 13.3% expansion of its regular portfolio.

Similarly, United Spirits (Diageo India), whose brand lineup includes Johnnie Walker, Smirnoff, McDowells and Godawan, saw its P&A segment volumes growing 5.4% in FY25, in sharp contrast to its popular segment contracting by almost 2%.

Companies have identified premiumization as one of their primary growth drivers.

Radico Khaitan, Piccadily Agro, John Distilleries and others have launched multiple brands in the luxury segment in whisky and gin categories. Multinational players like Pernod Ricard and United Spirits have launched or acquired Indian liquor brands, ICICI Securities noted. United Spirits has hived off a number of brands from the popular segment as a franchisee business to sharpen its focus on its premium portfolio.

In the beer industry, while the contribution of premium brands is comparatively lower (at around 12% compared to around 65% in whisky segment), over the last five years, premium beers have grown at ~7% compared to overall industry growth of ~2%.

“Demand in the P&A category is accelerating, supported by rising disposable incomes and urban lifestyle changes. This has boosted realisations and profitability for players focused on higher-end segments,” Anirudh Garg, partner & fund manager at INVasset PMS, told Mint.

Brokerage upgrades and renewed institutional interest have further buoyed valuations. Investors are factoring in long-term brand strength, improving margins, and favourable demographics.

“Overall, this rally reflects both cyclical recovery and structural tailwinds, positioning liquor stocks as standout performers in an otherwise defensive FMCG basket,” he added.

Taking a sip

Volumes are surging, consumers are in good spirits (literally) and are not hesitating to splurge on premium products and the runway for growth is considerable. So where’s the catch for investors?

Liquor perhaps is the only sector where the biggest risk lies not with companies but with the government.

Alcohol in India is a state subject, with production, distribution and sale of liquor coming under the ambit of state administrations. The interplay of fiscal pressures, socio-cultural climate and political calculations makes the operating environment incredibly complex. This also means every state and union territory effectively is an independent market with its own set of regulations on production, distribution and pricing.

This can mean sudden good or bad news for companies. For instance, earlier this year, Heineken-owned United Breweries, the maker of Kingfisher beer, suspended sales in Telangana, the country’s biggest beer market, over the state’s refusal to allow price hikes. (The sales were later resumed).

Similarly, Madhya Pradesh banned liquor sales in 19 religious cities, with the chief minister saying the state is mulling total prohibition.

View Full Image

On the other end of the spectrum, alcohol firms received a shot in the arm after Uttar Pradesh introduced a key reform in its excise policy, allowing liquor shops that previously sold either beer or spirits to operate as composite outlets permitted to sell both, resulting in doubling of the retail touch points for spirits from 6,500 outlets to roughly 12,500.

“While the liquor sector in India has long been viewed as opaque and tightly regulated, recent developments suggest a gradual shift toward greater transparency and structural reform. Several states are digitizing excise systems, streamlining licensing, and adopting modernized policies that reduce discretionary intervention and enhance predictability. For instance, Delhi is set to implement a revised excise framework by June 2025 aimed at improving transparency,” INVasset’s Garg said.

“However, the regulatory landscape remains inherently fragmented, with each state exercising significant autonomy over pricing, taxation, and distribution. Social sensitivities around alcohol also mean that periodic policy reversals or bans cannot be ruled out. While the industry is certainly becoming more organized and investor-friendly, regulatory overhang will remain a structural characteristic,” he added.

Another aspect to note is the high valuations of frontline stocks. For instance, Radico Khaitan and United Breweries trade at over 100-times earnings, while United Spirits trades at a P/E multiple of 65.

“Yes, the multiples look expensive, but if you factor in the earnings visibility and growth outlook for the future, they are more palatable,” Anand Rathi’s Thakur said. “On FY27 earnings basis, the stocks are expected to trade in the range of 55-60 times earnings, which is still on the higher side, but given the outlook, look reasonably priced,” he added.

The multiples look expensive, but if you factor in the growth outlook, they are more palatable.

— Ajay Thakur

Most analysts remain bullish on the sector on the back of the premiumization trajectory of the frontline companies. Additionally, the ban on advertising and the complex regulatory framework mean the entry barriers are high for new entrants.

“In our view, Radico Khaitan and Allied Blenders and Distillers are well positioned to benefit from this trend and are expected to witness accelerated growth in their premium portfolios. United Spirits is likely to maintain steady performance, given its already high exposure to premium brands,” ICICI Securities noted. However, it flagged the complex and volatile regulatory environment as a key risk.

Perhaps it is cosmic justice that alcohol policy swings mirror the after-effects of the product itself—unpredictable and prone to surprises. But for now, investors are savouring the buzz.

Key Takeaways

- The top two performing stocks in the Nifty FMCG index, over the past year, are Radico Khaitan and United Spirits.

- The stocks of smaller alcohol companies have jumped, too.

- Prices of raw materials, like extra neutral alcohol, are currently benign.

- Secondly, the premium portfolios of these companies are doing well, leading to robust margin expansion.

- Brokerage upgrades and renewed institutional interest have buoyed valuations.

- Investors are factoring in long-term brand strength and favourable demographics.

- But the multiples for some companies look expensive.

- Besides, the regulatory landscape remains fragmented—periodic policy reversals or bans cannot be ruled out.