Inside India’s SME IPO boom—and why it’s getting riskier MakkalPost

Many figured if they had to get stuck, it better be in a private, unlisted company. After years of being an overlooked corner of the market, SME listings are now catching eyes and stirring interest among investors.

The post-covid-19 pandemic era ushered in a new generation of investors, more risk-tolerant, less scarred by past market meltdowns. Simultaneously, regulatory tweaks made the SME space more inviting.

And nothing shows the shift better than the steady climb in listing gains.

Numbers don’t lie

In 2024, SME initial public offerings (IPOs) delivered an average pop of around 60% on debut, a figure that has only been rising over the past five years, according to Prime Database. 240 SME IPOs hit the market during the year, raising ₹8,761 crore, the highest in both number and funds raised since the pandemic.

The frenzy continued into 2025, despite market volatility. Tariff wars, between the US and China, geopolitical conflicts in West Asia, as well as the brief India-Pakistan war, played on the minds of investors. While large IPOs are being delayed, downsized, or even shelved, SME IPOs appear to be bucking the trend.

Here’s a telling sign of surging investor interest and risk appetite: Between 27 and 30 May alone, six SME IPOs opened for subscription. In May, 13 SME IPOs hit the market which is more than double the six new listings on the mainboard, data from Prime Database shows.

The IPO of Srigee DLM, a plastic injection molding company, which opened between 5 May and 7 May, saw hysterical demand—subscribed 490 times overall, with the retail portion booked 243 times and the non-institutional investor category over a staggering 1,500 times.

Earlier in January, Parmeshwar Metal, a copper wire rod manufacturer, hit the IPO market with a bang, too. Retail investors subscribed nearly 600 times, and non-institutional investors over 1,200 times.

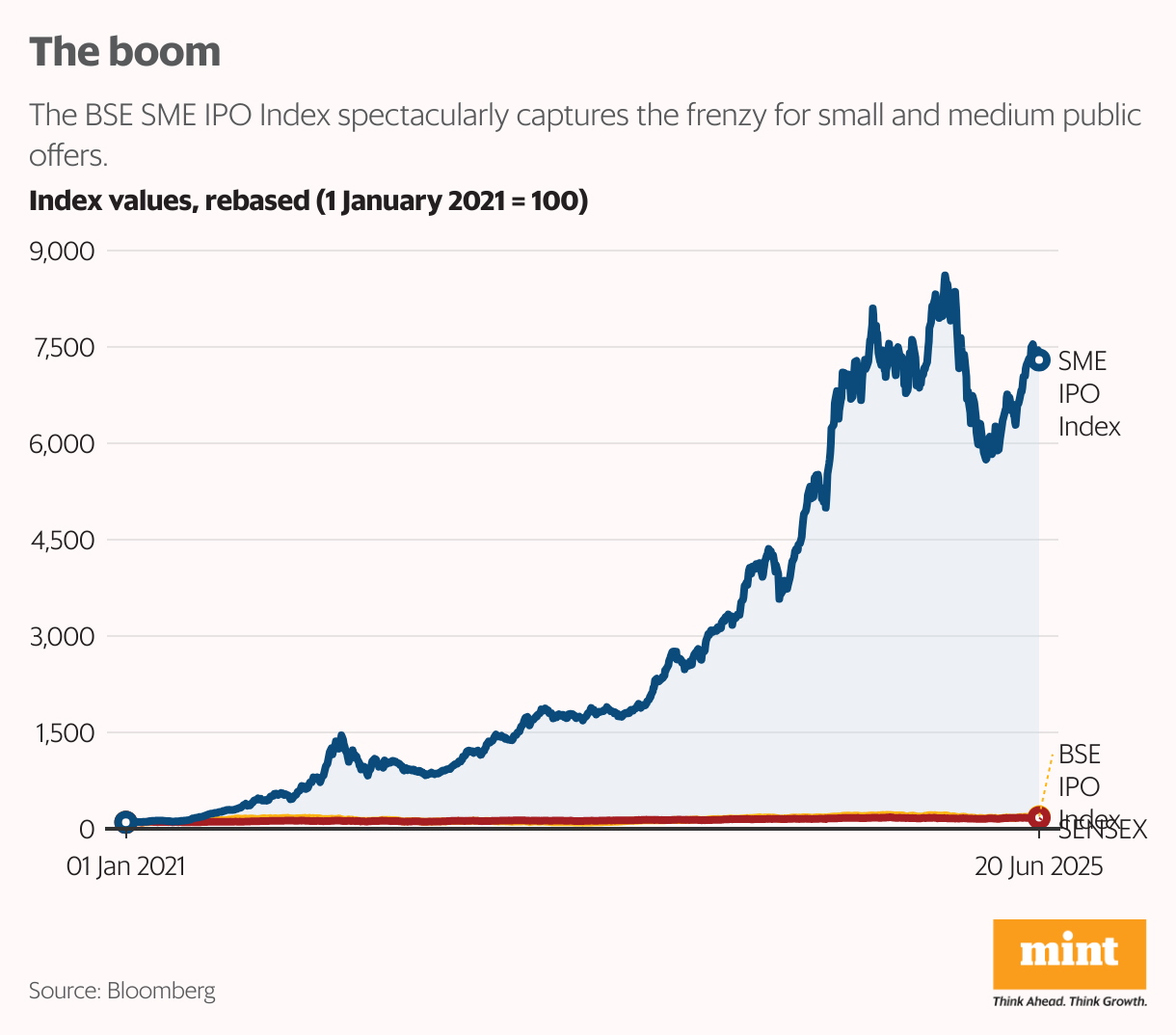

The S&P BSE SME IPO index captures this frenzy—it has shot up from 1,400 points in 2021 to over 100,000 points now (see chart).

Virtuous cycle?

Much of this frenzy is being driven by a self-reinforcing loop: early successes attract more retail and high net-worth investors, pushing up oversubscription levels and valuations.

“SME IPOs offer equity exposure with high-growth potential,” said Vishnu Agarwal, a seasoned IPO investor and founder of Stock Knocks, a platform offering information on unlisted and listed stocks.

He believes the ecosystem has matured in the last five to seven years. “A promoter running a business for 10–15 years may realize that continuing at their own pace might take another 20 years to scale up. But with equity capital, they could fast-track that growth within five years,” Agarwal said.

Still, the question looms: Is this meaningful capital formation or froth in disguise?

The SME exchanges–BSE SME and NSE Emerge–were launched in 2010. The Securities and Exchange Board of India (Sebi) stepped in two years later to simplify regulations for smaller firms. From March 2012 to October 2024, 745 SMEs had listed with a combined market cap of ₹2 trillion, according to a Sebi consultation paper dated 19 November 2024.

Unlike past bubbles, this boom is backed by real retail investors, better SME financials, and smarter regulations, making it a lasting shift, not just a passing trend, some believe.

Contrary to what some skeptics may claim, Tarun Singh, a former Sebi official and managing director of Highbrow Securities, sees India’s SME IPO boom representing a structural shift in the capital markets rather than a speculative bubble underpinned by stronger company financials. He pointed out that unlike past bubbles, this boom is backed by real retail investors, better SME financials, and smarter regulations, making it a lasting shift, not just a passing trend.

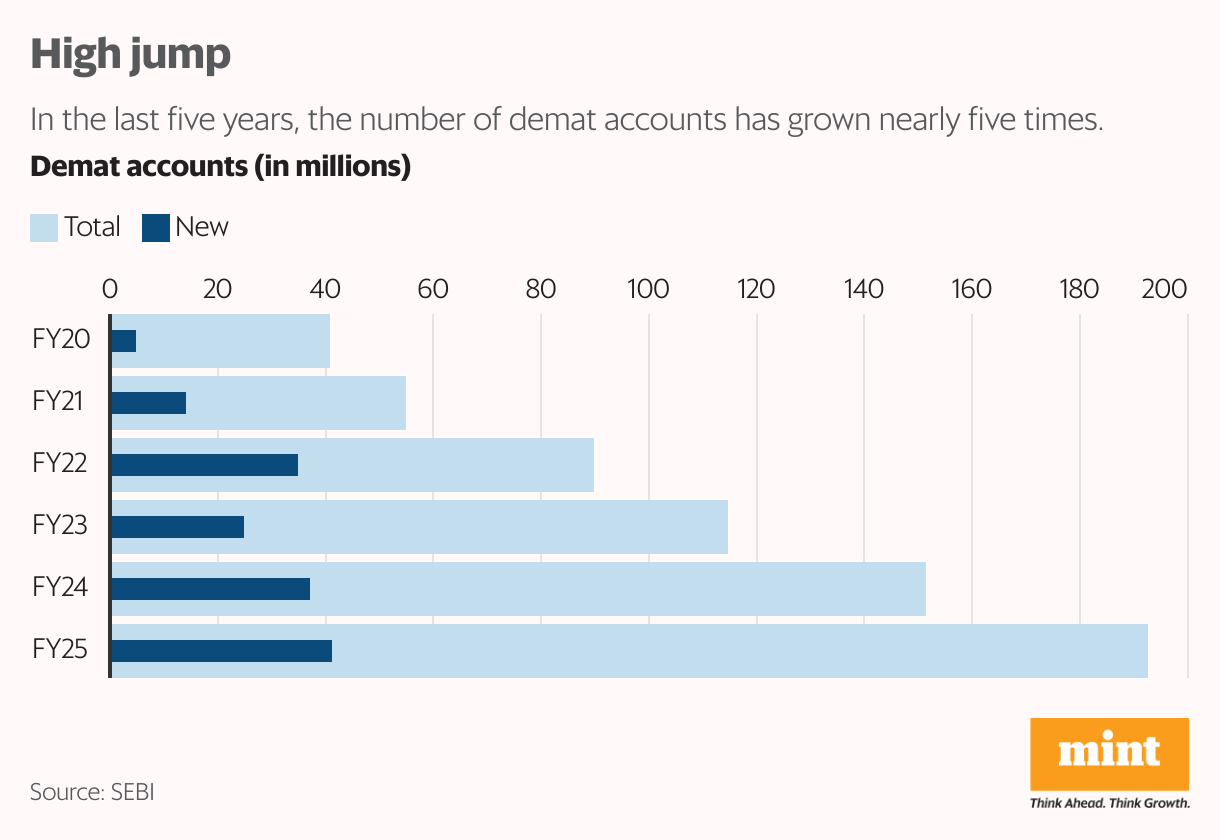

“Until late 2021, SME IPOs struggled to get even 1x subscription, but this changed dramatically in 2022 when the surge in demat accounts (crossing 90 million that year) directly correlated with a 2.5x jump in fundraising to ₹1,980 crores,” he said.

The trend accelerated through 2023-24, with demat accounts exceeding 140 million and SME IPOs regularly seeing 50-100x subscriptions, Singh highlighted.

Another reason driving the surge in SME listings is the growth potential these companies offer.

This potential has enthused investment companies. Bay Capital, for instance, is set to launch an SME fund under Category III, rather than Category I, Rahul Kumar Jha, principal at the company, said.

Category III mandates a significantly higher ticket size of ₹1 crore, in contrast to the ₹25 lakh threshold in Category I.

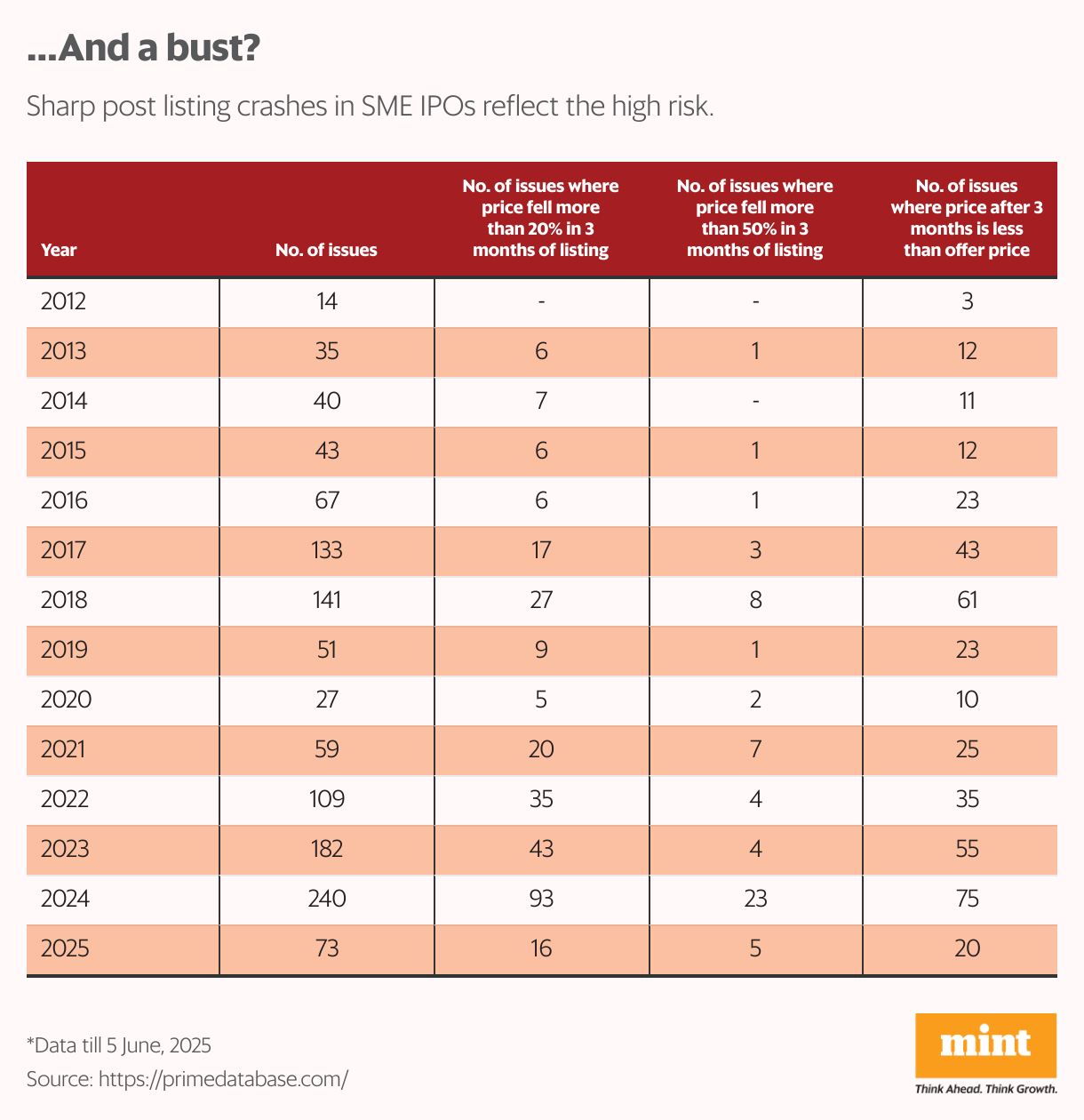

Nonetheless, in 2025 so far, 75 SME IPOs have hit the street and it has been a bit of a mixed ride. While 34 saw listing day gains, 41 listed in the red, data from Chittorgarh, a company that provides information on Indian financial markets, showed.

Jha, therefore, had a word of caution: the SME space is best suited for investors with a very high risk tolerance. “Only those who truly understand how to invest responsibly should consider entering this segment,” he emphasized.

Caveats and cracks

Some experts draw parallels with startups—both the segments often lack transparency, making it tough to find credible bets. This is where structured advisory and accountability become essential.

View Full Image

A major concern is the absence of a valuation cap at listing. Without guardrails, even questionable companies can go public, creating long-term damage to investor trust.

Arun Kejriwal, an investor and founder of Kejriwal Research & Investment Services, said that small issue sizes and tight allotments make SME stocks ripe for manipulation. “The allotment size in SME IPOs is small, which means the shares are concentrated in fewer hands. That makes it easier to manipulate the stock,” he said.

“In many cases, SME IPOs are priced at frothy valuations—sometimes more than 30 times what would be considered reasonable,” he added. “You’ll find similar or even larger companies on the mainboard trading at one-fifth or one-tenth the value. That’s telling.”

Some market experts were quick to point out that keeping valuations in check at the time of listing could help avoid sharp post-listing crashes.

To counter some of these risks, BSE Ltd claimed to have ramped up its scrutiny protocols to independently verify disclosures made in the draft red herring prospectus (DRHP). It even claimed to deploy artificial intelligence tools to scan filings for red flags.

“BSE is also engaging with merchant bankers to spread awareness about recent regulatory amendments,” a spokesperson told Mint. The exchange has additionally been conducting educational seminars across cities to inform SMEs about the regulatory landscape, “with a hope to see quality issues coming into the market,” the spokesperson added.

On the regulator’s flagged concerns around inflated valuations and potential price manipulation, BSE clarified that it seeks necessary explanations from companies and merchant bankers during document reviews to ensure proper disclosures. “The pricing of an issue is determined through a combination of factors such as the company’s growth prospects, industry trends, and prevailing market forces,” the exchange said.

According to Prime Database, 2024 saw 93 SME listings where share prices dropped over 20% within just three months. In 75 cases, the stocks slipped below their issue price in that same period. Even more striking, 23 listings plunged by 50% or more within three months of debut.

Lawyers working in the SME space said that the regulator, Sebi, cannot directly regulate the valuation of a company. “The aspect of valuation and its accuracy wholly depends upon the ecosystem supporting the IPO process and merchant bankers end up playing a crucial role in ascertaining the same,” Archana Balasubramanian, partner at Agama Law Associates, said.

Case for mainboard

Market experts advising SMEs believe that well-performing companies can consider moving to the mainboard after gaining experience on the SME platform. True wealth creation happens when SMEs graduate to the mainboard, unlocking substantial long-term value.

Priyanka Madnani, founder and chief executive officer (CEO) of Terex Ventures, which provides advisory services to SMEs, highlighted that 92 out of 100 SME companies “lack a concrete post-listing growth strategy”, which often leads to losses and ultimately erodes value for both stakeholders and investors. This is why most institutional investors favour mainboard over SME listings.

Yet, she believes that well-governed and strong SMEs have the potential to deliver 5x returns within three years of listing. Terex Ventures is preparing 24 such companies for IPOs between this year and next.

The missing link, according to Madnani, is robust risk analysis. “If an SME claims ₹300 crore turnover post-listing, where are the checks to validate that?” she questioned.

Experts recommend “handholding, education, and institutional support” to ease SMEs’ transition to public status.

Transformative story

Some SMEs view listing as more than capital-raising—it enhances governance and board-level transparency.

For Share Samadhan Ltd, which helps recover unclaimed investments, SME IPOs are a springboard for brand visibility and better governance. “It has brought a cultural shift. Our team now feels accountable not just to the business, but to public shareholders,” said the co-founder and chief executive officer Vikash Jain. The company’s shares were listed on 16 September 2024.

Going public was transformative, said Adit Bhatia, deputy general manager at Mach Conferences & Events Ltd, a company that provides meetings, incentives, conferences and events (MICE) solutions. An SME listing not just boosts credibility and unlocks growth capital, but as Bhatia explained, it also leads to “clients and vendors seeing us differently now, with much more confidence.”

Mach’s shares listed on the BSE SME exchange on 11 September 2024.

Experts note SMEs often struggle post-listing due to leaner teams and informal governance practices.“Adapting to financial reporting and audit committee demands, maintaining proper board procedures, and disclosing related party transactions can be overwhelming initially,” said Sanjay Israni, partner at Desai & Diwanji, a law firm.

Clients and vendors see us differently now, with much more confidence.

—Adit Bhatia

Others pointed to the difficulty of adopting the rigorous reporting standards of Sebi and the stock exchanges.

“One of the biggest challenges which comes is the formation of a structured board: moving from a promoter-driven to a board-driven governance model,” said Balasubramanian of Agama Law Associates.

Sebi tightens the leash

To address rising risks, Sebi has steadily tightened SME IPO regulations over the past five years.

Key reforms include raising the financial eligibility threshold and mandating a minimum of ₹1 crore in operating profits, limiting the offer for sale (OFS) component to 20%, enforcing promoter lock-ins, and ensuring that IPO funds are not used to repay promoter loans.

In December 2024, the minimum application size was raised to ₹2 lakh from ₹1 lakh previously, and the number of allottees increased to 200 from 50 earlier.

Regulatory enforcement has also intensified. Last month, Mint reported that Sebi barred Synoptics Technologies and Varyaa Creations, along with their merchant bankers, from misuse of up to 70% of IPO funds.

While Synoptics, which listed on 13 July 2023, sells network and infrastructure solutions, Varyaa Creations, whose shares listed on 30 April 2024, is a jewellery manufacturer.

View Full Image

An interim order from Sebi alleged that over ₹14 crore—about 70% of Varyaa Creations’ IPO proceeds—was diverted on the day of listing, directly from the public issue account to three entities, based on instructions from the lead manager, Inventure Merchant Banking Services Pvt. Ltd, without being routed through the company’s bank account.

In its board meeting of 18 December 2024, the market regulator flagged related party transactions (RPTs) as a major route for fund diversion among SME-listed entities and extended mainboard RPT norms to SMEs.

Despite these actions, the SME IPO space still faces significant structural issues.

Oversight or overkill?

Sebi’s new chairperson, Tuhin Kanta Pandey, recently asked exchanges and merchant bankers to step up scrutiny and cautioned investors that returns may not reflect real performance.

“You can’t have a system where merchant bankers walk away with 50% to 70% of IPO proceeds—how can any serious company participate when commissions are that steep? These are turning into non-performing investments,” said a former regulatory official who requested anonymity.

The official flagged misuse of IPO proceeds by shell companies as a persistent concern.

“Exchanges must tighten oversight, and merchant bankers need to act more responsibly. We can’t discourage credible promoters with a broken system,” the former official further added.

On the other hand, merchant bankers claim due diligence has intensified. SKI Capital Services, which managed four SME IPOs last fiscal year, plans six more in the coming fiscal. Its managing director, Narinder Wadhwa, said diligence became stricter after January this year.

However, Wadhwa believes the SME IPO space is somewhat over regulated. He pointed to Sebi’s guideline requiring companies to have a post-issue net worth or IPO size above ₹10 crore, arguing this limits access for many promising businesses.

“If we restrict too much, the whole purpose of the SME platform—which is giving smaller companies a non-banking route to raise capital—gets defeated,” he said. “While regulation is important, it shouldn’t choke innovation or early-stage entrepreneurship”.